Sending $1,000 across a border sounds simple. You give your bank the money, they send it to the other side, and the recipient gets it. Reality is a bit more complex.

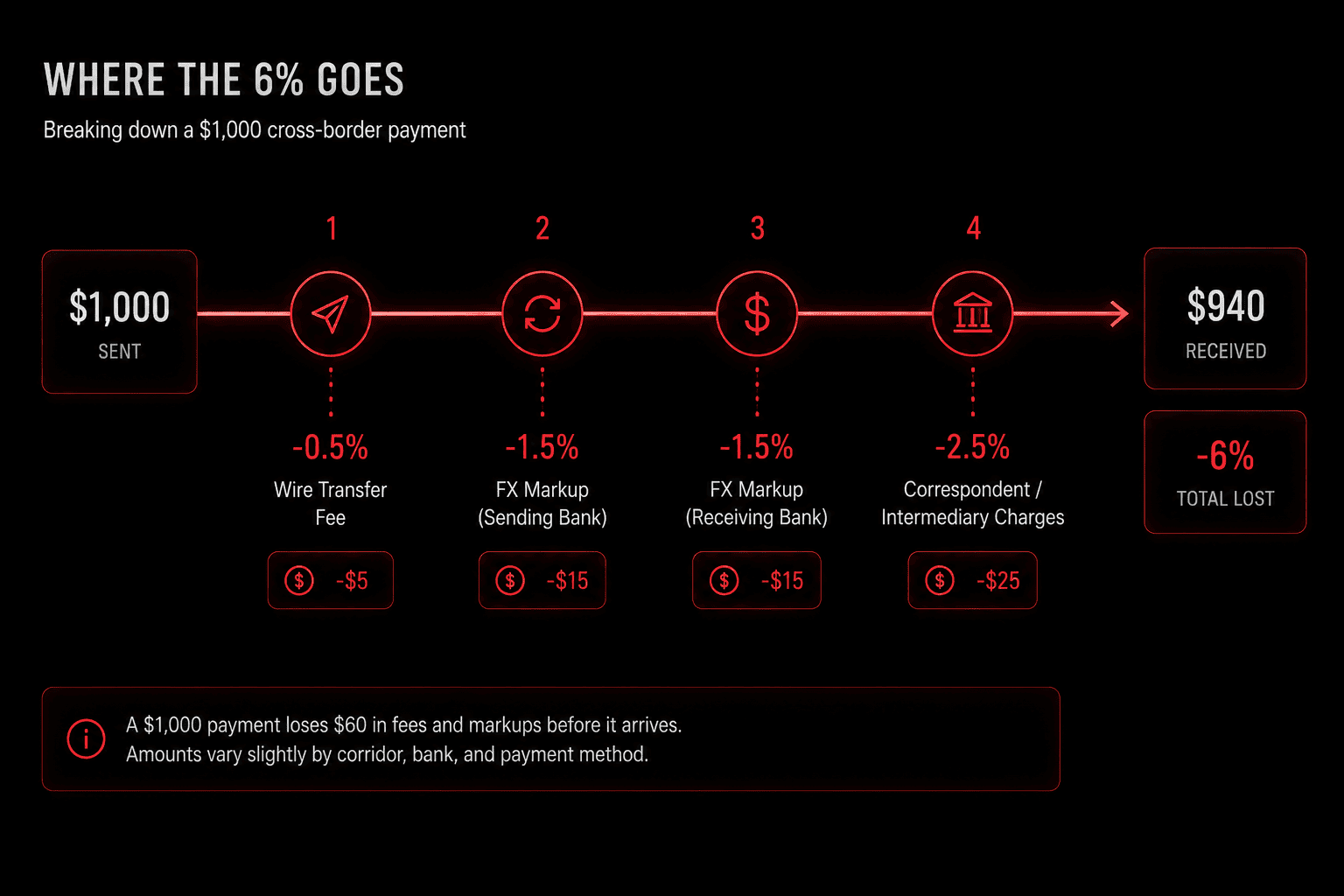

If you're sending that $1,000 from the US to family in the Philippines, you'll lose somewhere between $60 and $80 before it arrives. That's 6 to 8% gone to fees, currency markups, and intermediary charges. For remittances to low-income countries, the average sits at 6.35% per the World Bank's Remittance Prices Worldwide — a figure that has barely budged in years.

The cost isn't the only problem. The time is.

That $1,000 doesn't arrive in hours. It arrives in 3 to 5 business days, sometimes longer depending on which banks are involved and what time of day you send it. The recipient can't rely on having it when they need it. Your working capital is tied up in transit. If you're a small business doing international payroll or paying an overseas vendor, this matters.

The system works this way because moving money across borders isn't a simple transfer. It's a chain of intermediaries, each taking a cut.

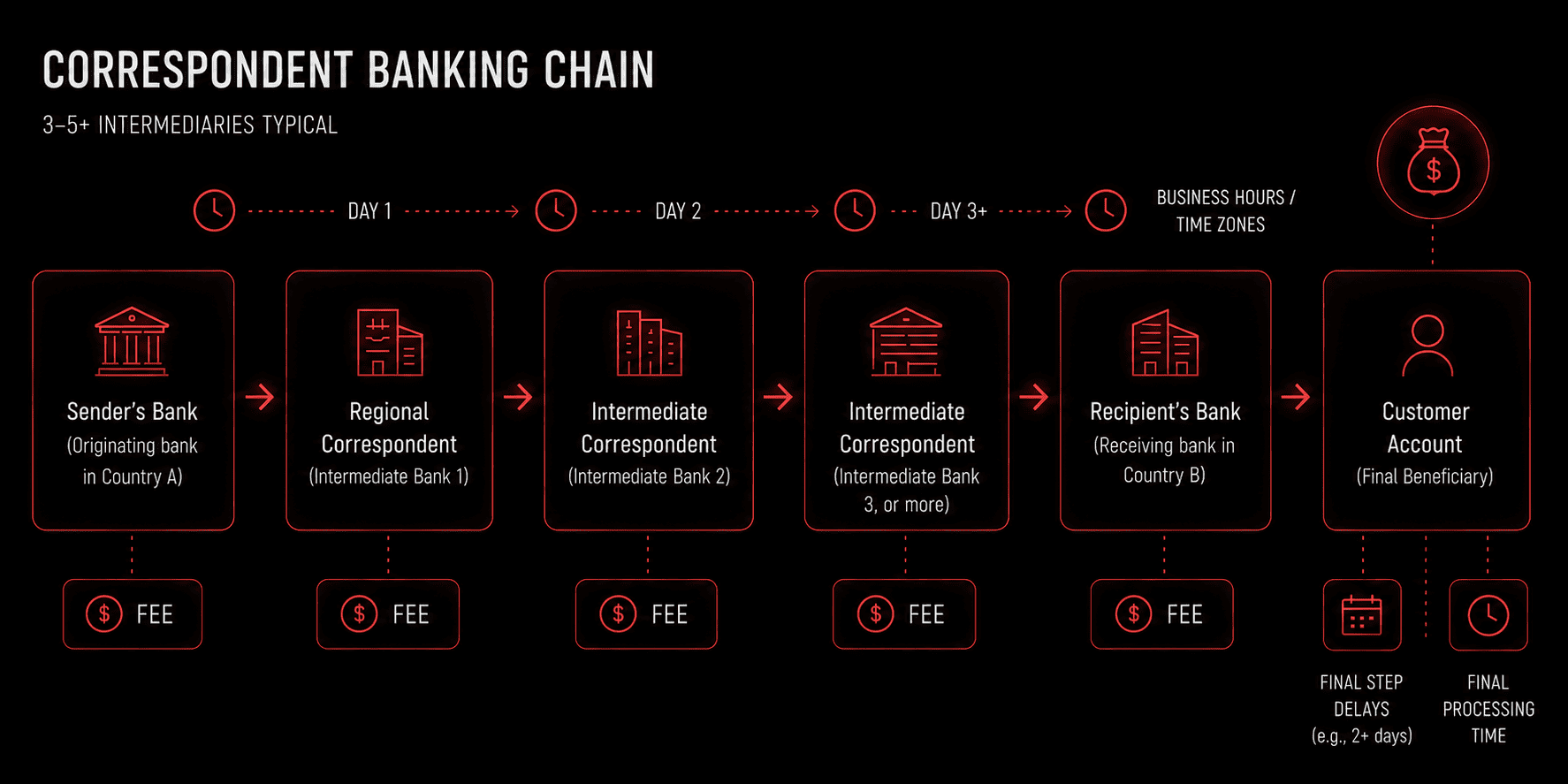

The cost breakdown

Here's what happens inside that 6%.

When you send $1,000 to another country, your bank doesn't send your money directly to the recipient's bank. Instead, it goes through a network of correspondent banks. Your bank has a relationship with a correspondent bank in a regional hub, which in turn has a relationship with another correspondent bank, which ultimately connects to the recipient's bank. Each one takes a fee.

On top of the wire transfer fees themselves, there's the currency conversion. Your bank quotes you an exchange rate that's not the real market rate. It's marked up by 1 to 5%. That's pure spread for the bank. Then the recipient's bank does the same thing on the other end. By the time the money lands, it's been converted twice through markups at each step.

These aren't small charges that add up to nothing. For a $500,000 international payment, even a 0.1% fee is $500. The annual volume of cross-border B2B payments worldwide is roughly $145 trillion. At typical rates of 2 to 7%, that represents tens of billions of dollars in costs annually — costs that don't buy anything or move anything faster.

Why does it take days?

The time delay compounds the cost problem.

When your bank initiates a SWIFT wire (the global standard for international bank transfers), it's sending a message through a network built in the 1970s and upgraded piecemeal ever since. The message travels. It waits for processing windows. If it arrives outside business hours in the destination country, it waits until business hours resume. If there's a holiday, it waits for the next business day. Currency conversions have their own settlement cycles. The recipient's bank then needs to confirm it received the money, reconcile it against its internal ledgers, and credit the account.

The theoretical minimum with modern SWIFT infrastructure is a few hours. The practical reality is 2 to 5 business days for most transfers, and longer if anything goes wrong.

For businesses, this creates a real problem: working capital is stranded in transit. If you're a manufacturer in Vietnam and you just paid a supplier in Germany, that money won't be back in your account for days. You can't use it, can't rely on it being there, can't forecast with certainty when you'll have access to funds. You might need to keep extra cash on hand just to account for the float.

For individuals sending remittances, the delay is a different kind of problem. If your family needs money urgently, you can't guarantee it will be there when they need it. The cost hits harder too, because you're often not sending large sums. A $500 remittance with a 6% fee means you sent $470 worth of value. The recipient gets the full $500, but $30 of your money vanished into fees and markups.

What blockchain promised

Blockchain technology emerged with a straightforward promise: remove the intermediaries.

Instead of moving money through correspondent banks, you move it peer-to-peer. No middlemen taking cuts. No SWIFT network with processing delays. No currency conversion through multiple banks. You send, the network confirms it, and the recipient has it. Done in minutes, and at a fraction of the cost.

The promise made sense, but the execution is where things broke down.

Why most blockchains didn't solve this

Bitcoin was the first blockchain, and it was designed to be a store of value. That's not the same thing as a medium of exchange. The transactions are slow, expensive to reverse, and designed around a 10-minute confirmation time. Good for locking in something you want to keep forever. Not practical for everyday payments where you need certainty in minutes and low fees matter.

Ethereum and other general-purpose blockchains followed, designed for running any kind of program on top of them. That flexibility is powerful, but it creates a problem for payments: to run anything on the network, you need to pay a fee that fluctuates with demand. When the network is busy, the fee spikes. You don't know what you're paying until after the transaction is confirmed. If you're a business processing customer payments, uncertainty is expensive. You can't confidently quote a price.

Both Bitcoin and Ethereum also require something called a "smart contract" to do anything interesting — a piece of code that runs on the blockchain itself. That code has to be stored on the network, executed by every validator, and secured against attacks. For simple payments, that's architectural overkill. It adds time and cost.

So blockchain technology existed, but it wasn't specifically designed for the cross-border payment problem. It was designed for other things, and payments were an afterthought.

What purpose-built payment infrastructure looks like

The question isn't whether blockchain can solve cross-border payments. It's what happens when you design a blockchain specifically for that problem rather than adapting a general-purpose network.

Purpose-built infrastructure makes different choices.

Instead of running code on the blockchain, it validates state changes. The logic runs on the client side — the sender's device or their bank's system — and the blockchain simply confirms that the transaction was valid and irreversible. That's faster and cheaper. You don't wait for the network to execute code and settle the result. You send the payment, the network confirms it in seconds, and it's final.

Instead of a variable fee that depends on network demand, a payment-focused blockchain can use an adaptive fee mechanism that keeps costs predictable regardless of transaction volume. You can quote a customer a price and be confident it won't spike unexpectedly.

Instead of a 10-minute block time or a 15-second settlement window, purpose-built infrastructure can settle transactions in seconds — not fast enough to break the laws of physics, but fast enough that working capital isn't meaningfully affected.

The fixed supply means no inflation eroding the value between when you send and when the recipient receives. If you send a dollar's worth of value, they get a dollar's worth.

And because it's designed from the ground up for payments, the entire architecture is focused on one goal: moving value across borders quickly, cheaply, and reliably.

The design matters

The 6% cost and 3 to 5 day settlement time aren't bugs in the current system. They're features of the architecture. Correspondent banking networks require intermediaries because they settle through the traditional banking system. SWIFT requires processing time because it was designed for a different era. Currency conversions require multiple exchange points because each intermediary needs to profit.

None of that changes unless the infrastructure changes. Blockchain can change it. Most blockchains haven't because they weren't built for this problem.

The ones that were built for payments from the very beginning operate under fundamentally different economics and timing. They settle in seconds, not days, and cost fractions of a percent.

That difference compounds. For an individual sending remittances, it means more money reaches the family. For a business making international payments, it means better cash flow and no working capital tied up in transit. For the global economy, it means trillions of dollars in transaction costs can be reduced to near-zero.

The problem is real. The solution exists. It just has to be built specifically for this, and for this alone.

Learn more about how eCurrency is built here.